Ace With Secondaries

We believe secondaries are one of the most effective ways to unlock liquidity, strengthen domestic ownership, and back India's breakout companies at scale.

Our secondaries fund has deployed ₹1,000+ Cr, backing India's marquee private companies at the moment risk/reward makes the most sense. We underwrite every deal from first principles, quality is never a casualty of deal velocity.

The Fastest Growing Asset Class

₹377B

India's secondary market reached ₹377 billion in FY25, up 32% from FY24. H1 FY26 has already recorded ₹361 billion, nearly matching the previous full year's deal value.

7.21 Years

Indian AIFs take an average of 7.21 years to achieve 1.0× DPI, highlighting why investors increasingly seek liquidity through secondary transactions.

3.7×

Average secondary deal size in India increased from ₹2.28 billion in FY20 to ₹8.39 billion in H1 FY26, reflecting a shift toward larger, more institutional transactions.

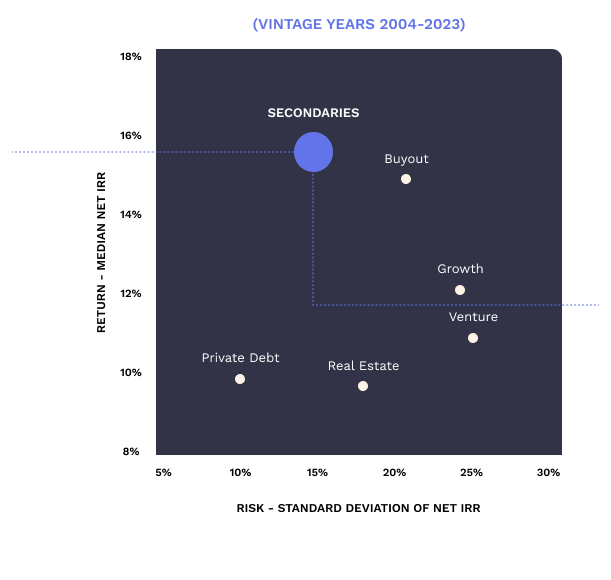

The Secondaries Edge

Risk-Return Profiles of Private Market Asset Classes (Global Data)¹

Secondaries deliver higher median net IRRs than buyout, growth, and venture, outperforming primary PE in every category

Standard deviation of net IRR for secondaries is around 15%, versus 20–25% for primary PE, offering lower risk exposure

Faster Liquidity

Capital comes back sooner through quicker distributions and earlier DPI.

Valuation Discipline

Pricing tied to demonstrated performance, not projections.

Exit Visibility

Clearer timelines and more predictable outcomes for capital return.

De-risked Growth

Exposure to proven companies with aligned long-term partners.

Timing is an

asset class.

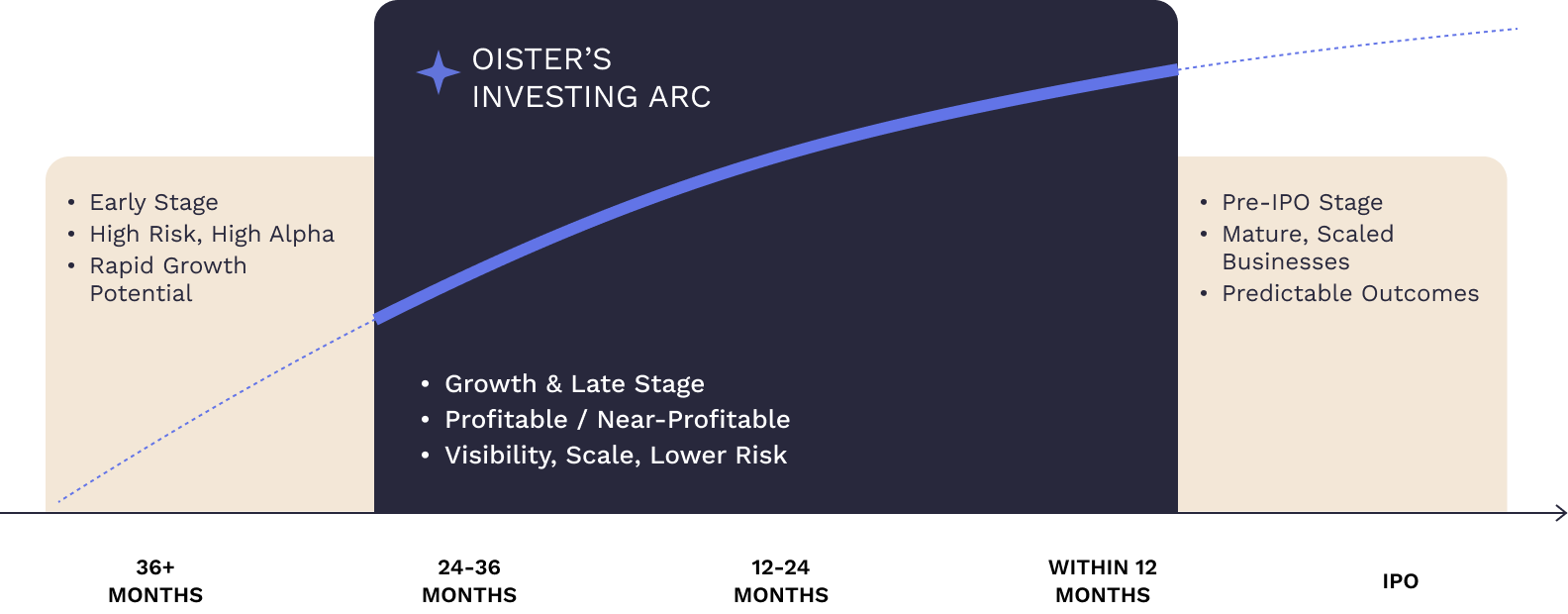

OISTER'S Investing Arc

A focused window to invest in proven businesses, with clear execution and visible paths to liquidity

For Long-Term

Investors

Oister's secondaries strategy is designed for institutions, family offices, and sophisticated investors seeking compounding with visibility and discipline.

We allocate at scale into India's breakout companies — profitable, near-profitable, and IPO-bound.

For Founders

Or GPs

The best companies don't wait until IPO to plan liquidity.

At Oister, we work with high-growth, profitable or near-profitable firms to create clean pathways 12-36 months before exit.

Our role is simple:

- Give early shareholders timely liquidity.

- Strengthen cap tables with long-term investors.

- Let founders keep building without compromise.

When the time is right, the best founders know where to turn.

India Is Ripe for Secondaries Breakout

A Decade of Capital, Waiting for Exits

Asia Turns to Secondaries, India Next in Line

India's DPI Gap and the Secondaries Solution

Your inside track on secondaries in India and worldwide

Learn how secondaries really work

Legal Disclaimer

DisclaimerThe information on the website of Oister Global is for informational purposes for creating awareness about private markets as a financial product and is not meant for sales, promotion or solicitation of business or investment. The funds mentioned herein are not being offered for sale or subscription but are being privately placed with a limited number of high net worth individuals, corporates, banks, financial institutions, social venture funds, foundations, societies, co-operative societies and such other persons who are permitted to invest under the regulations. The funds are prohibited from making an invitation to the public to subscribe to their units.

It may expressly be noted that the information contained herein does not constitute an offer to sell or a solicitation of an offer to buy the units of the funds described herein. Neither the fund(s), the investment manager, the trustee nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or completeness or contents of this website and the information herein, or, in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected that each prospective investor will pursue its own independent due diligence. In particular, without limitation to the generality of the foregoing, neither the fund(s) (represented by the trustee), the trustee, the investment manager nor any of their respective affiliates or representatives assume any responsibility for the accuracy of the statistical data and other factual statements concerning India and its economy contained in this website which have been obtained from publicly available documents or other sources considered reliable but which have not been prepared or independently verified by the fund(s), the trustee, the investment manager or any of their respective affiliates or representatives or their respective advisors. Certain information contained in this website constitutes "forward-looking statements," which can be identified by the use of forward-looking terminology such as "may," "will," "should," "expect," "anticipate," "target," "project," "estimate," "intend," "continue" or "believe," or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of the fund(s) may differ materially from those reflected or contemplated in such forward-looking statements. In making an investment decision, investors must rely on their own examination of the funds and the terms of the offering, including the merits and risks involved. These securities have not been recommended by any regulatory/statutory authority.